On 16 November 2021, SEBI had issued certain amendments to its master circular (no. SEBI/HO/CFD/DIL1/CIR/ P/2020/249 ) dated 22 December 2020 which laid down the framework of schemes of arrangement by listed entities. The amendments inter alia, required a No Objection Certificate (NOC) from lending scheduled commercial banks/financial institutions/debenture trustees to be submitted with the stock exchanges before the scheme is sanctioned by the National Company Law Tribunal (NCLT).

Regulation 37(1) of the Listing Regulations requires a listed entity desirous of undertaking a scheme of arrangement or involved in a scheme of arrangement to file the draft scheme of arrangement with the stock exchange(s) for obtaining the no-objection letter, before filing such a scheme with any Court or Tribunal, in terms of requirements specified by the SEBI or stock exchange(s) from time to time.

- Second and third proviso to clause (i) of section 80 of the Companies (Amendment) Act, 2017

- Section 56 of the Companies (Amendment) Act, 2020

SEBI through a circular dated 3 January 2022 has clarified that the NOC required from lending scheduled commercial banks/financial institutions/debenture trustees should be submitted before the receipt of the no-objection letter from the stock exchange in terms of Regulation 37(1) of the Listing Regulations.

To access the text of master circular number SEBI/HO/CFD/DIL1/CIR/ P/2020/249, please click here

To access the text of circular dated 16 November 2021, please click here

To access the text of the circular dated 3 January 2022, please click here

On 24 January 2022, SEBI notified certain amendments to the Listing Regulations, the key amendments are listed below:

-

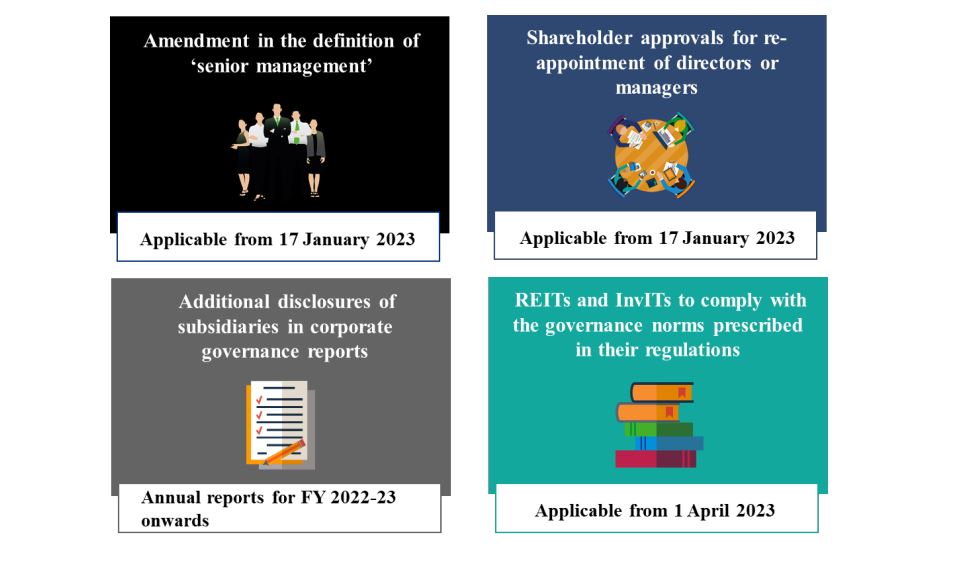

Appointment of directors (Regulation 17): As per the amendments, approval of shareholders is required for appointment of a person on the Board of Directors (BoD) or as a manager at the next general meeting or within a time period of three months from the date of appointment, whichever is earlier. (Emphasis added to highlight the change)

Further, the amendments require that the appointment or a re-appointment of a person, including as a managing director, whole-time director or a manager, who was earlier rejected by the shareholders at a general meeting, shall be effected only with the prior approval of the shareholders. In this regard, the statement annexed to the notice to the shareholders under Section 102(1) of the Companies Act, 2013, shall contain a detailed explanation and justification by the Nomination and Remuneration Committee (NRC) and the BoD for recommending such a person for appointment or re-appointment. - Statement of deviation(s) or variation (Regulation 32): Where the listed entity has appointed a monitoring agency to monitor the utilisation of proceeds of a public or rights issue, the monitoring report of such an agency shall be placed before the audit committee on a quarterly basis (earlier required on an annual basis), promptly upon its receipt.

- Transfer or transmission or transposition of securities (Regulation 40): Transmission or transposition of securities held in physical or dematerialised form shall be effected only in dematerialised form.

- Effective date: The amendments are effective from the date of their publication in the official gazette i.e., 24 January 2022.

To access the text of SEBI notification, please click here

Action points for auditors

-

Auditors that issue compliance certificate with regard to compliance of conditions of corporate governance by listed entities will need to verify whether:

- Appointment of managers has taken place by obtaining the assent of shareholders within the prescribed timelines

- A prior approval of shareholders has been obtained for appointment or reappointment of a person, including as a managing director, whole-time director or a manager, who was earlier rejected by the shareholders at a general meeting, along with a detailed explanation by the NRC and BoD for recommending such a person.

The Securities and Exchange Board of India (SEBI) recently amended regulation 23 of the SEBI (Listing Obligations and Disclosure Requirement) Regulations, 2015 (Listing Regulations) with regard to related party provisions. This regulation, inter alia, mandated entities with listed specified securities (i.e., equity shares and convertible securities) to submit to the stock exchanges disclosure of Related Party Transactions (RPTs) in the format specified by SEBI within the prescribed timelines. Recently, SEBI vide a circular dated 22 November 20211 prescribed the disclosure obligations, including the format to be used by issuers of specified securities for reporting of RPTs to stock exchange. This circular is applicable from 1 April 2022.

In addition to the issuers of specified securities, High Value Debt Listed Entities1 (HVDLEs) are also required to submit the RPT disclosures (as prescribed under regulation 23 of the Listing regulations). This disclosure has to be provided along with the standalone financial results for half year on a ‘comply or explain’ basis up to 31 March 2023 and on a mandatory basis post 31 March 2023. However, the format to be used by HVDLEs for such disclosures was not specified. SEBI through a circular dated 7 January 2022 has clarified that the provisions of SEBI circular dated 22 November 2021 which specifies disclosure obligations of entities that have listed their specified securities in relation to RPTs will be applicable to HVDLEs.

- HVDLEs are those entities which have listed non-convertible debt securities and have an outstanding value of listed non-convertible debt securities of INR 500 crore and above. As per recent SEBI circulars, HVDLEs are required to comply with all corporate governance provisions on a ‘comply or explain’ basis upto 31 March 2023 and on a mandatory basis post that.

To access the text of amendments to Regulation 23 of Listing Regulations, please click here

To access the text of SEBI circular dated 22 November 2021, please click here

To access the text of SEBI circular, please click here

Action points for auditors

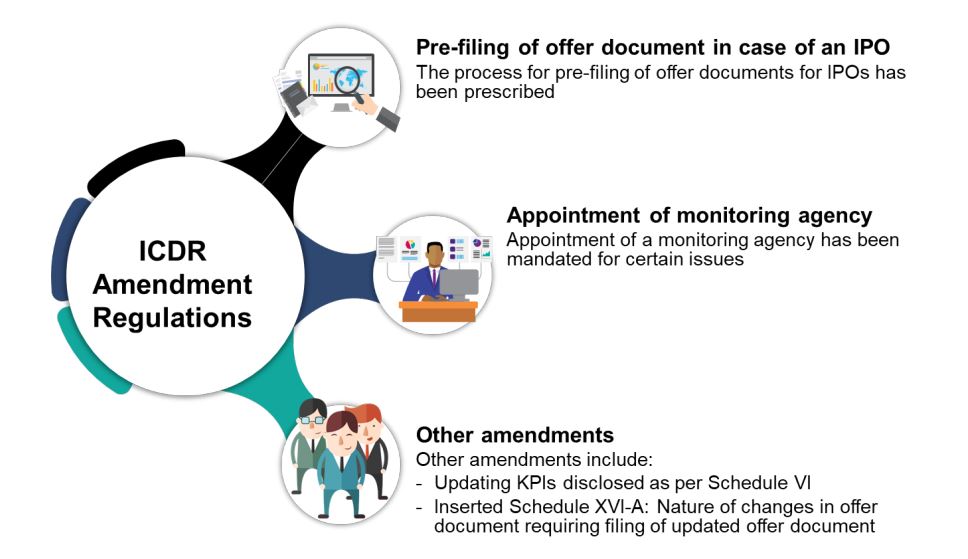

While performing audit procedures on related party transactions, auditors of HVDLEs could also refer to the half-yearly disclosures made to SEBI under regulation 23 of the Listing Regulations, to the documents and explanations submitted to the audit committees and shareholders with regard to the material related party transactions.On 14 January 2022, SEBI notified various amendments to the SEBI (Issue of Capital and Disclosure Requirements) Regulations 2018 (ICDR Regulations)4. These amendments to ICDR regulations (amendments) have been issued to tighten rules for an Initial Public Offering (IPO). Some of the key amendments include:

-

Cap on the usage of the issue proceeds for unidentified future acquisitions (Regulation 7): The ICDR regulations specify the general conditions that need to be ensured by an issuer making an IPO. The amendments have introduced a cap on usage of issue proceeds, where issue has been raised for:

- general corporate purposes and

- such objects where the issuer has not identified acquisition or investment target.

The cap on the usage of issue proceeds as a percentage of the amount being raised by the issuer is as under:

- 35 per cent on an overall basis for both these purposes

- 25 per cent for objects where the issuer has not identified acquisition or investment target.

However, such limits would not apply if the proposed acquisition or strategic investment object has been identified and specific suitable disclosures about such acquisitions or investments are made in the draft offer document and the offer document (effective from 14 January 2022)

-

Restriction on the number of shares that can be offered for sale by significant shareholders: (Regulation 8A): The amendments have inserted regulation 8A, which restricts the number of shares that can be offered for sale by certain shareholders, where draft offer document is being filed by an issuer without track record (i.e. under regulation 6(2) of the ICDR regulations). As per regulation 8A:

- Sale by persons, holding more than 20 per cent of the pre-issue shareholding of the issuer, should not exceed 50 per cent of their respective pre-issue shareholding. Further, provisions of lock-in5 would be applicable to such shareholders

- Sale by persons, holding less than 20 per cent of the pre-issue shareholding of the issuer, should not exceed 10 per cent of their respective pre-issue shareholding (effective from 14 January 2022)

- Extension of anchor investors' lock-in period to 90 days in certain cases (Clause 10(j) of Schedule XIII-Part A): Before amendment, the ICDR regulations mandated a 30 days lock-in period for shares allotted to the anchor investors from the date of allotment. The amendments now require a lock-in of 90 days on 50 per cent of the shares allotted to the anchor investors from the date of allotment. On the remaining 50 per cent of the shares allotted to the anchor investors, there would be a lock-in of 30 days from the date of allotment. (This amendment is effective from 1 April 2022 for issues opening on or after 1 April 2022)

- Requirement of valuation report in certain circumstances (Regulation 166A- new regulation): The amendments have inserted regulation 166A to the ICDR regulations. As per this regulation, in case of a preferential issue wherein there’s a change in control or allotment of more than 5% of the post-issue share capital of the issuer company to an allottee, in a such case valuation report from a registered independent valuer would be required (effective from 14 January 2022)

- Requirement of reasoned recommendation from a committee of independent directors wherein preferential issue results in change in control of the issuer (Regulation 166A- new regulation): The amendments have inserted regulation 166A to the ICDR regulations. As per this regulation, in case of a preferential issue wherein there’s a change in control of the issuer, a committee of independent directors would be required to provide a recommendation along with their comments on all the aspects of preferential issue. Also, voting pattern of such a committee would be required to be disclosed to the shareholders (effective from 14 January 2022)

- Utilisation of funds of the issue to be monitored by credit rating agencies (Regulation 41(2)): As per the amendments, credit rating agencies would now be permitted to act as the monitoring agency with respect to the utilisation of the funds of the issue, instead of Scheduled Commercial Banks and Public Financial Institutions, as specified earlier. In addition to this, the monitoring agency would submit its report to the issuer on a quarterly basis, till 100% (earlier 95%) of the proceeds of the issue, excluding the proceeds raised for general corporate purposes, have been utilised (effective from 14 January 2022)

- Certificates to be issued by practicing company secretary (Regulation 163(2)): Certificate issued by a practicing company secretary is required to be placed before the general meeting of the shareholders considering the proposed preferential issue, certifying that the issue is being made in accordance with requirements of the ICDR regulations. (earlier, certificate was required to be issued by the statutory auditor of the issuer) (effective from 14 January 2022)

- Audits permitted by a Chartered Accountant (Schedule VI): As per ICDR regulations, the audited Consolidated Financial Statements (CFS) of the issuer and certified proforma financial statements of material subsidiaries or businesses material to the issuer are required to be disclosed in the offer document in certain cases. The audit or certification as prescribed was earlier required to be done by the statutory auditor of the issuer. The amendments now require the audit or certification (as the case may be) to be done by either the statutory auditor(s) or Chartered Accountants who hold a valid certificate issued by the Peer Review Board of ICAI (effective from 14 January 2022).

Effective date: These amendments are effective from the date of their publication in the official gazette, i.e. 14 January 2022. Certain amendments as prescribed in the circular would be effective from 1 April 2022 for issues opening on or after 1 April 2022.

- The amendments have been issued by the SEBI (ICDR) Amendment Regulations, 2022.

- Provisions of lock-in have been prescribed within regulation 17 of the ICDR regulations.

To access the text of SEBI notification, please click here

Action points for auditors

The amendments have brought a significant change in the scope of work of statutory auditors, mainly due to:

- Practicing company secretaries are now required to issue certificate to shareholders under the ICDR regulations, certifying that the issue is being made in accordance with requirements of the ICDR regulations.

- Any Chartered Accountant (whether or not the Chartered Accountant is appointed as a statutory auditor of the issuer) with a valid certificate issued by the Peer review board of ICAI can audit and certify the financial statements disclosed in the offer document

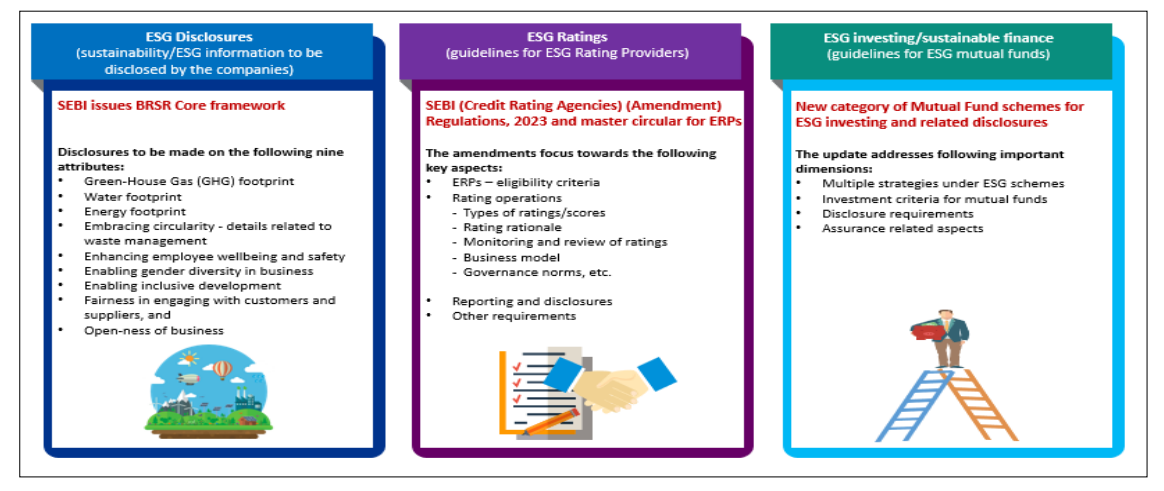

ESG rating providers (ERP) are typically not subject to regulatory oversight at present, this could lead to lack of trust in such ESG ratings. Therefore, there arises an imperative need, to ensure that the providers of such products operate in a transparent and regulated environment that balances the needs of all stakeholders.

SEBI, through a consultation paper, is seeking public comments on a proposed regulatory framework to regulate ERPs and oversight there on. This consultation paper follows a series of discussions held with multiple stakeholders, including global and national ERPs, credit rating agencies, mutual funds offering ESG schemes, and research/audit firms.

Comments on this consultation paper are invited upto 10 March 2022

To access the text of SEBI consultation paper, please click here

Action points for auditors

Auditors may emphasise the importance of this consultation paper to their clients, as ESG ratings will now be permitted to be obtained only from accredited ERPs, and products offered by ERPs would be as proposed in the consultation paper.